The Federal Reserve System was created in 1913 through the Federal Reserve Act, which President Woodrow Wilson signed into law on December 23, 1913. The public explanation was stability: the United States had suffered repeated banking panics, including the Panic of 1907, where bank runs, failed banks, frozen credit, and financial chaos exposed the weakness of the American banking system. The Fed was presented as the solution: a central banking structure that could provide a more stable currency, act as a lender of last resort, supervise banks, and prevent the banking system from collapsing every time panic spread through markets.

But the source layer was not clean. Before the Federal Reserve Act, a secret 1910 meeting at Jekyll Island, Georgia brought together powerful banking and political figures to develop the foundation for what became central banking reform. Federal Reserve History describes that meeting as a secret gathering that “laid the foundations for the Federal Reserve System,” while the Richmond Fed explains that the Jekyll Island plan involved a reserve association with regional branches governed by boards elected by member banks, with larger banks receiving more voting power. That matters because the Federal Reserve was not born purely from democratic public design. It emerged from panic, elite banking pressure, congressional negotiation, and a power struggle over who would control credit.

The racial undertone is also part of the structure. The Fed was created in 1913 America, during the Jim Crow era, before modern civil rights protections, before fair housing law, before equal access to credit, and before the banking system seriously confronted racial exclusion. The Federal Reserve Act did not need to say “racial exclusion” for the system to operate inside a racially distorted economy. Black Americans were already excluded from many wealth-building channels, and later generations faced redlining, discriminatory lending, predatory credit, and unequal access to banking. Even Federal Reserve-linked research acknowledges that Black Americans were subjected to redlining and discriminatory lending practices, while the Fed’s own history notes that fair-housing enforcement against racially motivated redlining did not arrive until after the Fair Housing Act of 1968.

In simple terms, the Federal Reserve works like the control room of the money-and-credit system. It does not print every dollar into existence by hand, and it does not directly set every price in the economy, but it influences the cost and availability of money. It sets key interest-rate policy, influences bank reserves, affects lending conditions, supervises parts of the banking system, buys and sells securities, and sends signals that move markets. When the Fed raises rates, borrowing becomes more expensive. Mortgages, credit cards, business loans, car loans, and investment decisions can all feel the pressure. When the Fed lowers rates or adds liquidity, borrowing becomes easier, asset prices can rise, and money moves more freely through the system. The official mandate says the Fed should promote maximum employment, stable prices, and moderate long-term interest rates, but those terms are broad, interpretive, and not self-defining.

This is where the usury problem enters the pattern. The modern banking system is built around interest-bearing money. Banks borrow, lend, charge interest, profit from credit, and expand economic activity through debt. The Federal Reserve sits above that structure as the central bank that influences the cost of money itself. So when the public hears “inflation,” they are usually told a simple story: prices are rising, and the Fed must fight them. But the deeper structure is more complex. The same institution that helps govern money, credit, bank liquidity, and interest rates presents itself as if it is merely responding to inflation from the outside. That is a distortion. The Fed is not just watching the fire. It helps design the monetary environment where the fire spreads, cools, or gets redirected.

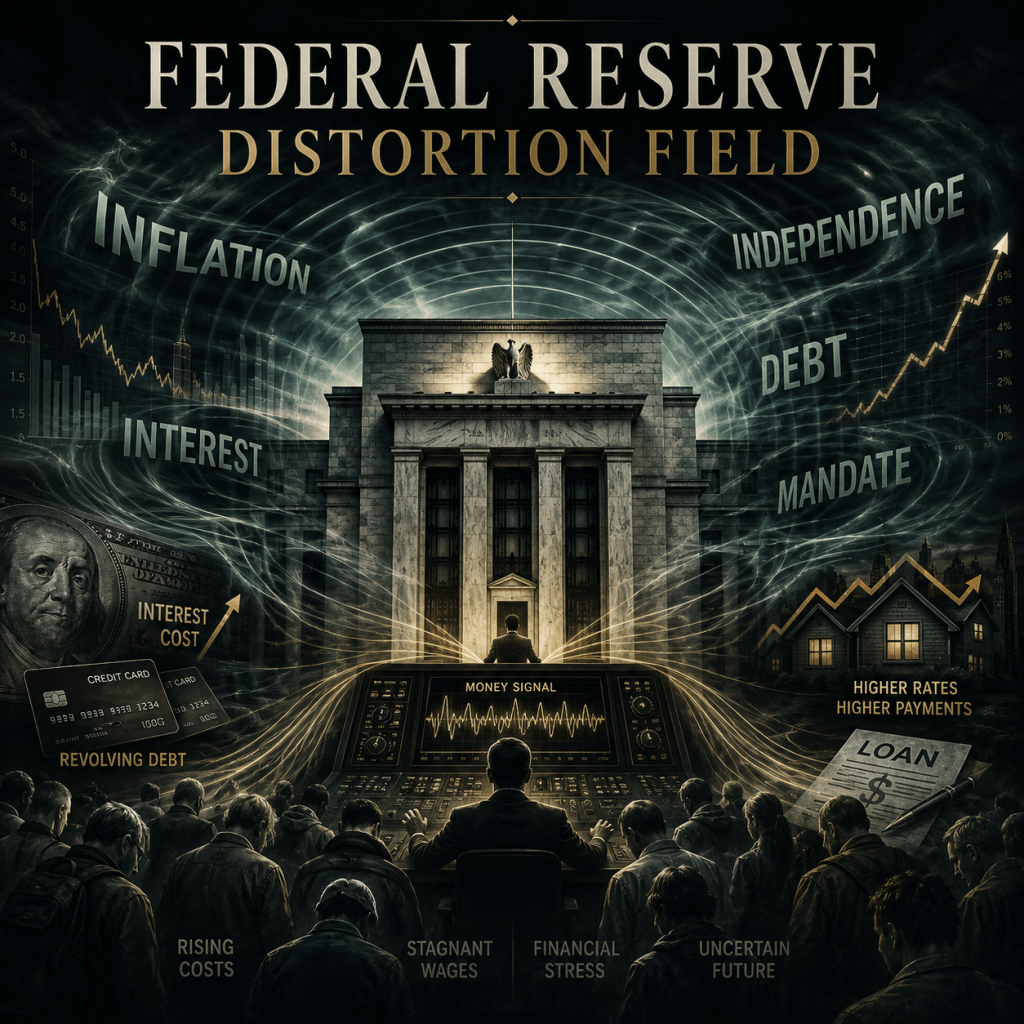

The biggest distortion is terminology. Words like inflation, price stability, monetary policy, independence, and dual mandate make a debt-and-interest control system sound like neutral economic weather management. The public hears technical language, but experiences rent pressure, mortgage pressure, credit-card pressure, wage pressure, grocery pressure, business pressure, and debt pressure. Crown State of Mind’s Federal Reserve distortion analysis describes this as a Hod–Yesod failure mode: technical explanations lose clarity at the representation layer, then become distorted through media, markets, politics, and public transmission before reaching lived reality.

Key Federal Reserve Distortions

Inflation Distortion

Inflation is presented as a general rise in prices, but the term often hides the specific forces behind price pressure: credit expansion, corporate pricing power, housing capture, supply shocks, government spending, energy costs, debt structures, money supply, and interest-rate policy.

Independence Distortion

The Fed is described as independent to protect monetary policy from short-term politics, but independence can become insulation when a powerful institution remains difficult for the public to correct.

Mandate Distortion

The Fed’s mandate sounds clear, but “maximum employment,” “stable prices,” and “moderate long-term interest rates” are broad terms that require interpretation. Congress wrote the words, but the Fed gives those words operational meaning.

Usury Distortion

The system normalizes interest-bearing money as technical finance, while ordinary people experience debt as survival pressure. The moral issue is hidden behind economic vocabulary.

Neutrality Distortion

The Fed presents itself as a neutral stabilizer, but its decisions affect winners and losers: banks, borrowers, asset owners, workers, renters, homeowners, investors, and businesses do not experience rate policy the same way.

Public Accountability Distortion

The Fed is formally accountable through congressional oversight, reporting, testimony, audits, and statutory authority, but the public experiences the institution as remote because its decisions are technical, delayed, and difficult to trace.

Banking Stability Distortion

The Fed is justified as a stabilizer of the banking system, but that framing can prioritize financial-system stability over household stability. Banks get emergency liquidity language. People get inflation language.

Signal Distortion

Fed communication moves through FOMC statements, market reactions, media interpretation, political attacks, investor forecasts, and public confusion. By the time the signal reaches everyday people, it often arrives as anxiety rather than clarity.

Democratic Distance Distortion

The Fed was created by Congress, but the people do not vote directly for Fed governors. The public lives under the outcomes, while corrective mechanisms remain slow, indirect, and elite-mediated.

Technical Language Distortion

Terms like “quantitative easing,” “restrictive policy,” “soft landing,” “liquidity,” “price stability,” and “market expectations” compress real economic pain into language that sounds clean, controlled, and expert.

The Contradictions

The first contradiction is that the Federal Reserve is defended as independent from politics, but it is deeply political in consequence. Interest rates affect housing, jobs, wages, loans, business survival, bank profits, asset values, and public trust. A decision that changes the cost of money is not politically neutral just because it is made by economists instead of elected officials.

The second contradiction is that Congress created the Fed, but Congress can blame the Fed when the system becomes painful. Congress created the institution, wrote the mandate, and preserved the structure. The Fed interprets and executes the mandate. The courts may protect its independence. Then the public is told to treat the outcome as technical necessity rather than a designed governance structure.

The third contradiction is that the Fed claims to fight inflation while operating inside an interest-bearing monetary system that puts debt at the center of economic life. The public is told inflation is the enemy, but debt, interest, and credit dependency remain normalized as the operating field.

The fourth contradiction is that Fed independence is treated as stability, while public accountability is treated as a threat. That reveals the value hierarchy. Market confidence receives protection. Public frustration receives explanation. Banks receive liquidity tools. Households receive lectures about inflation expectations.

The fifth contradiction is that the Fed is described as public-serving, but the groups that benefit most from its independence are often those closest to capital: major banks, financial institutions, asset holders, institutional investors, and market actors who can interpret Fed signals quickly and position themselves before ordinary people even understand what changed.

The sixth contradiction is that the Fed’s power depends on public trust, but its language often destroys public intelligibility. A system cannot claim legitimacy forever if the people affected by its decisions cannot clearly understand how the system works, who benefits, who pays, and how correction happens.

Who Benefits Most?

The people who benefit most from Federal Reserve independence are not ordinary citizens trying to understand why rent, mortgages, food, credit cards, and business costs keep rising. The primary beneficiaries are the institutions and actors closest to the money signal: banks, markets, major investors, financial firms, asset holders, and political actors who know how to convert Fed language into positioning.

That does not mean every Fed action is corrupt. The cleaner source-fidelity point is sharper: a system does not need to be openly corrupt to be structurally distorted. If power, language, credit, interest, and accountability are misaligned, distortion becomes the operating condition.

The Federal Reserve is not merely an economic institution. It is a 1913 power structure where public authority, private banking influence, interest-bearing money, legal insulation, market management, and democratic distance all meet inside one system.

The distortion is not only in what the Fed does. The distortion is in how the institution is described.

Public mandate.

Private pressure.

Interest-bearing control.

Legal protection.

Economic consequence.

Limited public correction.

All hidden under the clean word: independence.

Royal Politics is an independent political consulting and strategy platform built to examine power beyond the political performance.

Book a Strategy Session with Royal Politics

Need help turning a political issue into a strategy? Book a session with Royal Politics to discuss your goal, issue, campaign, or public-positioning need.

Leave a comment